Sharp EL-733 EL-733A Operation Manual - Page 34

pause

|

View all Sharp EL-733 manuals

Add to My Manuals

Save this manual to your list of manuals |

Page 34 highlights

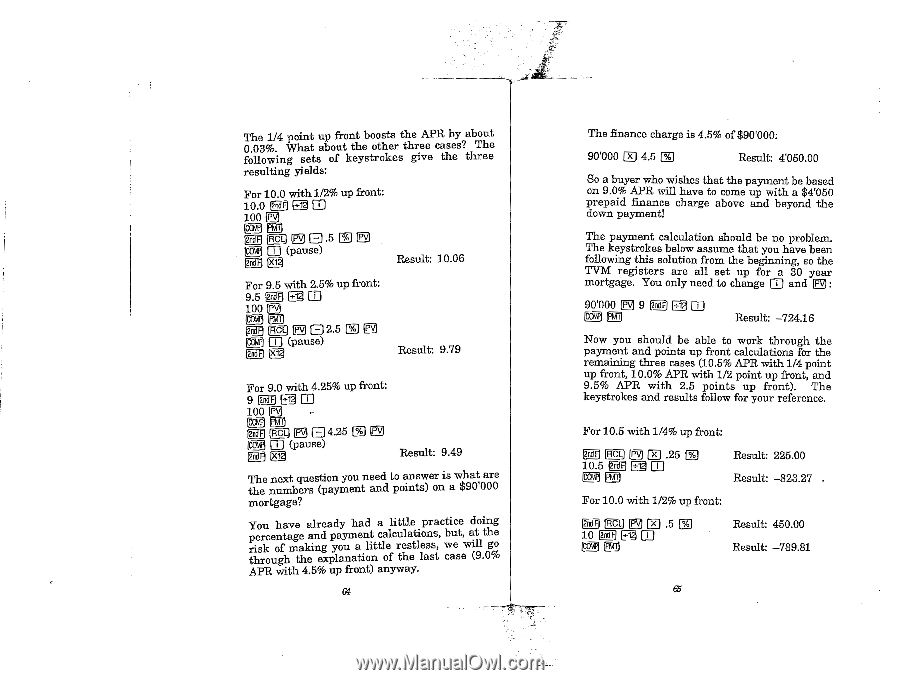

The 1/4 point up front boosts the APR by about 0.03%. What about the other three cases? The following sets of keystrokes give the three resulting yields: For 10.0 with 1/2% up front: 10.0 Iznd21 F -!1 W 100 IN NT) 12ndFl (nal El .5 U Pali 0 (pause) (x14 Result: 10.06 For 9.5 with 2.5% up front: 9.5 12ndFll÷121 QI 100 [2ndF) cQ Rv EJ 2.5 el Fvl [caw) n (pause) Fill) lx14 Result: 9.79 For 9.0 with 4.25% up front: 9 12ncIFJ I÷11 100 [NI 1 11 I?ndFl IFICL1113q [J4.25 VA Pv 03 13 (pause) 2nill X14 Result 9.49 The the next question you need numbers (payment and to answer is what are points) on a $90'000 mortgage? You have already had a little practice doing percentage and payment calculations, but, at the risk of making you a little restless, we will go through the explanation of the last case (9.0% APR with 4.5% up front) anyway. 64 The finance charge is 4.5% of $90'000: 90'000 Ex 4.5 VA Result: 4'050.00 So a buyer who wishes that the payment be based on 9.0% APR will have to come up with a $41050 prepaid finance charge above and beyond the down payment! The payment calculation should be no problem. The keystrokes below assume that you have been following this solution from the beginning, so the TVM registers are all set up for a 30 year mortgage. You only need to change EJ and 90'000 (W 19 2nd. I÷12) M (QT) Result: -724.16 Now you should be able to work through the payment and points up front calculations for the remaining three cases (10.5% APR with 1/4 point up front, 10.0% APR with 1/2 point up front, and 9.5% APR with 2.5 points up front). The keystrokes and results follow for your reference. For 10.5 with 1/4% up front: oar (Pa 113 El .25 W 10.5 Oar) (÷14 gT I l Result: 225.00 Result: -823.27 For 10.0 with 1/2% up front: (ROL) 0 C) .5 (2ndF) )444 m Result: 450.00 Result: -789.81 65

-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

|

|