Casio FC-200V User Guide - Page 61

Conversion Mode

|

UPC - 079767167004

View all Casio FC-200V manuals

Add to My Manuals

Save this manual to your list of manuals |

Page 61 highlights

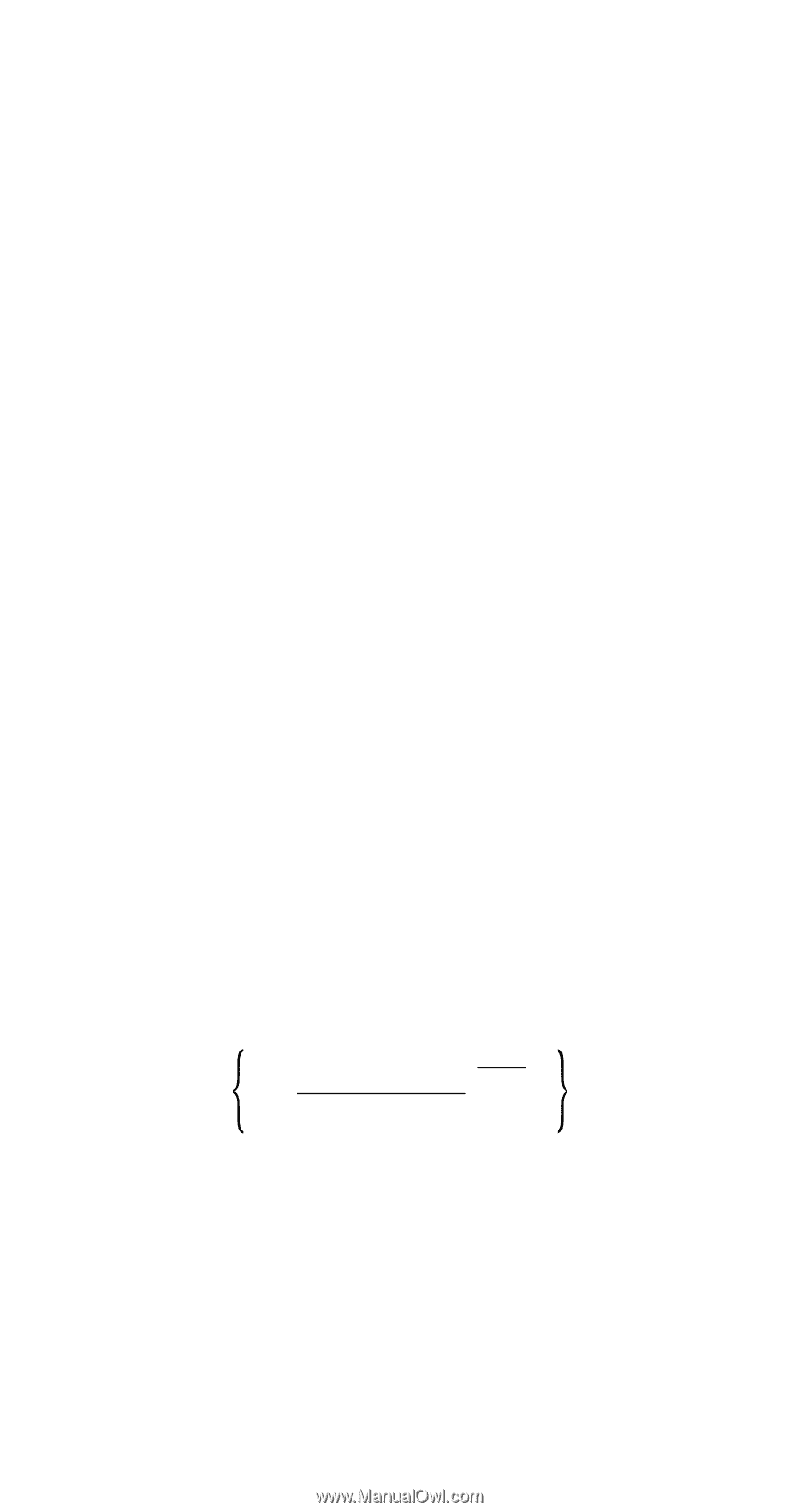

A Calculation Formulas a: Interest portion of payment PM1 (INT) INTPM1 = I BALPM1-1 × i I × (PMT sign) b: Principal portion of payment PM1 (PRN) PRNPM1 = PMT + BALPM1-1 × i c: Principal balance upon completion of payment PM2 (BAL) BALPM2 = BALPM2-1 + PRNPM2 d: Total principal paid from payment PM1 to payment PM2 (ΣPRN) ΣPM2 PRN = PRNPM1 + PRNPM1+1 + ... + PRNPM2 PM1 e: Total interest paid from payment PM1 to payment PM2 (ΣINT) • a + b = one repayment (PMT) ΣPM2 INT = INTPM1 + INTPM1+1 + ... + INTPM2 PM1 BAL0 = PV Payment: End (Setup Screen) INT1 = 0, PRN1 = PMT ... Payment: Begin (Setup Screen) Converting between the Nominal Interest Rate and Effective Interest Rate The nominal interest rate (I % value input by user) is converted to an effective interest rate (I %´) for installment loans where the number of annual payments is different from the number of annual compoundings calculation periods. { }[C / Y ] I%' = (1+ I% )[P / Y ]-1 ×100 100 × [C / Y ] The following calculation is performed after conversion from the nominal interest rate to the effective interest rate, and the result is used for all subsequent calculations. i = I%'÷100 k Conversion Mode • The Conversion (CNVR) Mode lets you convert between the nominal interest rate (APR) and effective interest rate (EFF). E-59

-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

|

|