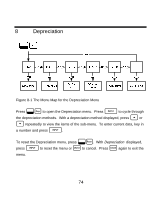

HP 20b HP 20b Calculator Quick Start Guide - Page 70

Yield, Price, Accrued, Actual/Cal.360, Annual/Semiannual

|

UPC - 883585875344

View all HP 20b manuals

Add to My Manuals

Save this manual to your list of manuals |

Page 70 highlights

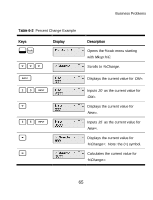

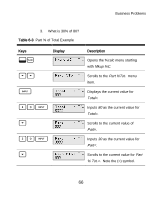

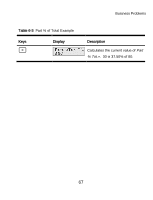

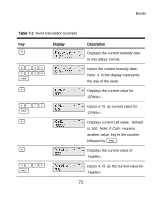

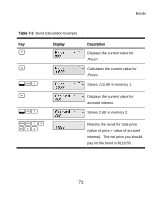

Bonds Table 7-1 Bond Menu Variable Call= Yield%= Price= Accrued= Actual/Cal.360 Annual/Semiannual Description Call value. Default is set for a call price per $100.00 face value. A bond at maturity has a call value of 100% of its face value. Note: Input only. Yield% to maturity or yield% to call date for given price. Note: Input/Output. Price per $100.00 face value for a given yield. Note: Input/Output. Interest accrued from the last coupon or payment date until the settlement date for a given yield. Note: Input/Output. Actual (365-day calendar) or Cal.360 (30-day month/360-day year calendar). Bond coupon (payment) frequency. What price should you pay on April 28, 2010 for a 6.75% U.S. Treasury bond maturing on June 4, 2020, if you want a yield of 4.75%? Assume the bond is calculated on a semiannual coupon payment on an actual/actual basis. See 70

-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

|

|