HP 113394 User Guide - Page 192

Modified Internal Rate of Return

|

UPC - 808736340502

View all HP 113394 manuals

Add to My Manuals

Save this manual to your list of manuals |

Page 192 highlights

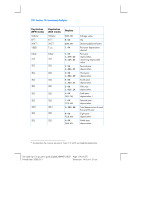

192 Section 13: Investment Analysis Modified Internal Rate of Return The traditional Internal Rate of Return (IRR) technique has several drawbacks which hamper its usefulness in some investment applications. The technique implicitly assumes that all cash flows are either reinvested or discounted at the computed yield rate. This assumption is financially reasonable as long as the rate is within a realistic borrowing and lending range (for example, 10% to 20%). When the IRR becomes significantly greater or smaller, the assumption becomes less valid and the resulting value less sound as an investment measure. IRR also is limited by the number of times the sign of the cash flow changes (positive to negative or vice versa). For every change of sign, the IRR solution has the potential for an additional answer. The cash flow sequence in the example that follows has three sign changes and hence up to three potential internal rates of return. This particular example has three positive real answers: 1.86, 14.35, and 29. Although mathematically sound, multiple answers probably are meaningless as an investment measure. This Modified Internal Rate of Return procedure (MIRR) is one of several IRR alternatives which avoids the drawbacks of the traditional IRR technique. The procedure eliminates the sign change problem and the reinvestment (or discounting) assumption by utilizing user stipulated reinvestment and borrowing rates. Negative cash flows are discounted at a safe rate that reflects the return on an investment in a liquid account. The figure generally used is a short-term security (T-Bill) or bank passbook rate. Positive cash flows are reinvested at a reinvestment rate which reflects the return on an investment of comparable risk. An average return rate on recent market investments might be used. The steps in the procedure are: 1. Calculate the future value of the positive cash flows (NFV) at the reinvestment rate. 2. Calculate the present value of the negative cash flows (NPV) at the safe rate. 3. Knowing n, PV, and FV, solve for i. File name: hp 12c pt_user's guide_English_HDPMF123E27 Page: 192 of 275 Printed Date: 2005/8/1 Dimension: 14.8 cm x 21 cm

-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

|

|