Sharp EL733A EL-733A Operation Manual - Page 20

Sharp EL733A Manual

|

View all Sharp EL733A manuals

Add to My Manuals

Save this manual to your list of manuals |

Page 20 highlights

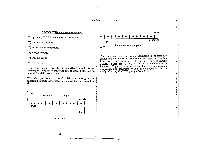

are that each month a certain amount of interest will be added to that account, INCREASING the account balance. THE CASH-FLOW SCILEDUL The amount of interest you receive each month depends on the balance of the account during that month including interest that has been added in previous months. Interest This is a cash-flow schedule. It represents an investment in a savings account. earns interest. And that is why it's called "compound interest." Compound interest is periodic. It is very committed to a 1.5% 1= month 119.56 certain period of time. To borrow from a well worn phrase: time, in financial calculations, is of the essence. In fact, you must know the compounding period of a loan or investment before you start. This is one variable about an 12 3i 1-100.00 i5 i6 17 18 19 110 111 I12 investment that has to be a known, because the whole calculation is based on it. The compounding period is One hundred dollars is invested at 1.5% per month (18% usually specified or assumed (very often it's monthly). APR compounded monthly) and left for one year. At the end of that year, when it is withdrawn, it has grown to 119.56. Once you know the compounding period of a loan or (Notice that the 18% APR here is just the monthly rate investment, you also have to know that the compounding multiplied by 12. This is sometimes called the "nominal period has one interest rate associated with it. You don't APR.") have to know what the rate is (it can be your unknown), but have to recognize that it's the interest rate associated with Understanding the cash-flow schedule is important when the compounding period that causes money to change in value at the end of each period. doing any type of financial calculation. The more complicated the calculation, the more necessary it is to kq draw a cash-flow schedule so that you have a clear picture But enough generalizations. Let's look at something a little in front of you when you key in the numbers. more pictorial. Notice on the previous cash-flow schedule that the periods are all regular (monthly) and that the interest rate per month is specified. Now to get a picture of how interest compounds, here are three cash-flow schedules that are shortened versions of the $100.00 savings investment.

-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

|

|