Sharp EL733A EL-733A Operation Manual - Page 32

institution

|

View all Sharp EL733A manuals

Add to My Manuals

Save this manual to your list of manuals |

Page 32 highlights

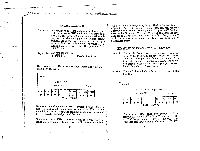

a month. Is it likely that this person will be able to find the financing to cash you out? Solution: If an institution were to loan your prospective buyer the cash, this is the situation that institution would be looking at (from the lenders perspective). PMT = 700.00 t2 t3 t 1=? PV = - 70'000 FV = 0 358 t 359 t 360 t 0=30 x 12 Would the return (or interest rate) be high enough in this case? If the calculated rate is about what the market is currently bearing, you may have a buyer for your house. First, make sure your calculator is out of BGN mode by pressing BGN to make the BGN indicator turn off. Then press: (Mode: FIN) 30 j2ndF] VIZ E) 0 E 70'000 +1- E 7001 Result: 0.97 This is the monthly rate. To compare it with the advertised rates multiply by 12 to get a nominal APR of 11.63%. At the time of this writing, that is a reasonable rate on a mortgage (perhaps even a little high) so your prospective buyer will likely be able to get financing. "POINTS UP FRONT" (PREPAID FINANCE CHARGES Nowadays, it is almost the norm to have to pay some finance charges up front in order to secure a loan, especially a mortgage. In the U.S., the FHA (Federal Housing Act) rates are well known for their dependence on the "points" that you are willing to pay up front. These "points" are percentage points. The more percentage points of the borrowed money you are willing to pay at the onset of the loan, the lower the rate will be that is used to calculate your payment. Prepaid finance charges or "points up front" have the effect of increasing the actual interest rate that is paid on the borrowed money. These prepaid finance charges reduce the net amount of money borrowed up front, without reducing the payment. This is not the same as a "down payment," which reduces both the money borrowed and the payment amount.

-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

|

|