Sharp EL733A EL-733A Operation Manual - Page 58

%APR+12

|

View all Sharp EL733A manuals

Add to My Manuals

Save this manual to your list of manuals |

Page 58 highlights

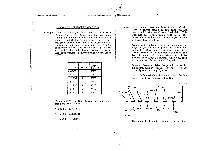

(For more details on sliding cash-flows with the TVM functions, you may want to review page 100.) You can think of INN as though it treats each cash-flow as a separate loan. In the previous example, if you slide just the first $6'000 cash-flow to the front of the time line, adjusting it for the interest rate, the cash-flow schedule would look like this: 1=18%APR(+12) 10'000 10'000 10'000 6'000 6'000 t 5487.25 ill t 111 i I I I I I I I I I IHI I I I I I I I I I I I till year 1 year 2 year 3 By sliding the first $6'000 cash-flow back six periods and adjusting for the 1.5% periodic interest rate, you reduce its value (you discount it) to about $5487.25. Next if you slide the first $10'000 cash-flow to the front of the time line, it looks like this: I 8'616.67 5487.25 'MIMI "N., year 1 18% APR (÷ 12) 10'000 i t 6'000 10'000 ill 61000 f 10'000 ill ' II II IIII I 11111 III 7\,, ,, V. V year 2 year 3 Then, slide the next $10'000 cash-flow to the front: 8'489.33 8'616.67 5487.25 i= 18% APR (+ 12) 10'000 6'000 10'000 6'000 10'000 /\. year-1 year 2 year 3 Notice that, because it is slid back one period farther than the first $10'000 cash flow, the second $10,000 cash-flow is worth less up front. .112 113

-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

|

|