Sharp EL733A EL-733A Operation Manual - Page 27

Explanation

|

View all Sharp EL733A manuals

Add to My Manuals

Save this manual to your list of manuals |

Page 27 highlights

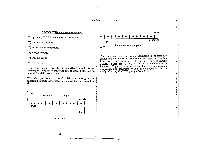

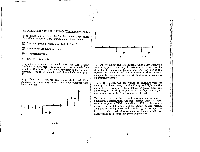

PV CALCULATIONS Example: Referring to the last example (and with your calculator set to FIN mode and the display at (--) El), the buyer tells you that an affordable payment on the mortgage loan (which doesn't include taxes and insurance) would be right around $800.00. What does the price of the house have to be to reduce the payment from I $859.85 to 800.00? Keystrokes: 800 f+/-I M W 12000 E Result: 99456.61 Explanation: The new situation looks like this on a cash-flow schedule: 1 PV=? you don't have to rekey everything. That is the real beauty of playing "what if' on the EL-733A. You can ask yourself questions like, "What if the payment changes to 800.00; how does that affect the PV?" and, "What if the interest rate changes to 11.2% APR; how does that affect the payment?" And the answers to those questions are just a few keystrokes away. EXAMPLES OF PV AND PMT CALCULATIONS Example: You are in the market for a new car. You are going to trade in your old car and you can afford about a $300 per month car payment . The interest rates are at about 12% APR. What can you afford to borrow on a car if you get a 4 year loan? How about a 5 year loan? Solution: The cash-flow schedule for the 4 year loan looks • like this: i =10.5-i- 12 I), n=30 x 12 FV = 0 'Mtn i3,54t5t51:57t51:51:61 PMT = -800.00 Now you know the payment (PMT is specified to be -800.00), and you need to calculate a new present value (PV). To this new PV, you need to add the amount of the down payment to arrive at the desired price of the house. Once you have a TVM situation keyed in, if you want to make just one change to see how it affects another value, w PV = ? = 12 + 12 =1% per month n=4 x12 FV 0 tHl 143 14, 4 jer15 PMT = -300.00 1:711;18 The amount (PV) that you borrow will be completely paid off WV = 0) in 48 months (n = 48) at $300.00 per month (PMT = -300.00). The interest rates you estimate to be around 12% APR 51

-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

|

|