Sharp EL733A EL-733A Operation Manual - Page 72

iora2E0, 100E7.2

|

View all Sharp EL733A manuals

Add to My Manuals

Save this manual to your list of manuals |

Page 72 highlights

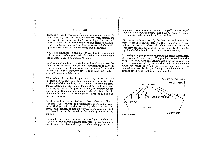

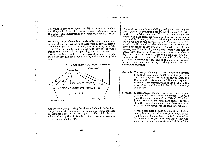

180 = 0.39, so n = 12.39. The cash-flow schedule should look something like this: FV .103.60 BGN Mode 039 t PMT .3.60 t 2t i= 10 +2 11 tip PV = PRICE + (1 - 0.39) 3.60 Because the coupon payments start at the beginning of the first whole period, this is a BGN mode calculation, so the FV contains both the redemption value and the last coupon payment. This boils down to a simple PV calculation where n is not an integer: (Mode: FIN) BGN mode should be on. 120iora2E0 100E7.2 w2E] PMT. Ei 100 ID 0 WTI El (+/-I 01u170 M180 El Pawl 0 Result: -89.48 You will have to pay $89.48 for this bond to get a 10% yield-to-maturity. But that $89.48 is the price plus the accumulated coupon payment for the current period. For the formal "price" of the bond, subtract that accumulated coupon payment using the following keystrokes: 4x-ii 180070 M180 M3.6 MOE Result: -87.28 The price of the bond is $87.28. If you know the price of a bond and you wish to calculate the yield of the bond, you can get pretty close to an answer using the EL-733A. However, you can't solve for yield directly. The following keystrokes give you an estimate of the yield to maturity if the price of the bond in the above example is $91.33. 3.6 [Fivr1170 M180 E]1+1-I QX [rum !rico OrgE191.33 Ell+/-1 12 El ICS) M Result: 3.83 13 IBGNI IM (End mode)Result: 3.70 The true semi-annual yield lies in between these two rates. You can make guesses at the true yield and then calculate the price as you did in the above example. When the keystrokes result in the correct price, you've arrived at the correct yield. Multiply by 2 to annualize the yield. Remember, if the purchase date falls on the coupon date, price and yield calculations are simple i and PV calculations and you don't have to deal with partial periods. 140 141

-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

-

79

-

80

-

81

-

82

-

83

|

|