Sharp EL733A EL-733A Operation Manual - Page 26

EX12 N2nd E[XVI

|

View all Sharp EL733A manuals

Add to My Manuals

Save this manual to your list of manuals |

Page 26 highlights

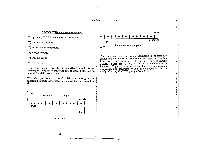

divide it by12. Notice that the Pm F) 1÷11 function is provided above the Dl key for this exact purpose. The periodic rate is the only one that makes any sense to the calculator. PV = 94'000.00 i =10.5 +12 Also, along with the nominal APR that they divide by 12 n=30x12 FV 0 and use in their calculations, most lenders are required to quote the effective APR or true APR which is a calculated 35$454354p$59 ,1,601? annual rate that includes compounding (and finance charges). For now, don't try to use effective rates in your calculations. Calculating effective rates is covered on PMT = ? pages 72 and 90. PAYMENTS AT THE BEGINNING OF THE PERIOD Your EL-733A can be set to solve TVM problems with The amount financed completely paid off (FV is = 0) $94'000 (PV over a period = of 94'000) 30 years to or be 360 months at a information periodic interest rate of 0.875% is all there and, after reading per the month. The explanation to this point, you should understand most of the subtleties payments at either the beginning or the end of the about this mortgage problem. cash-flow period. The only reason that this is mentioned here is because if you have your calculator set to BGN mode, you will not be able to get the right answer in this Tcahseh-ffollolwowsicnhgekdeuyles.troMkaeks esosluvreeftohrethBeGpNayinmdeicnat tionr tihsenaobtoovne example. The 7 key is used to switch the calculator in in your display: and out of BGN mode. When the display indicator BGN is turned on, the calculator is set to solve TVM problems assuming payments occur at the beginning of the period. Keystrokes: 106'000 12'000 E N 10.5 PH 1-.-121 EJ 30 land9 X12 E io Why should it make any difference if the payments occur at 0 the beginning or at the end of the period? Well, think about LiLff,,a Result: -859.85 it.... The quicker the balance is reduced, the less interest is going to accumulate and the smaller the payment. So in this problem, be aware that your calculator should not be in BGN mode when you are solving for this mortgage Naroetisceeptahraattethfeun2cndt9io[n-Os2Iaabnodve2ntdhe[XLVUI fuanncdtioFnis keys provided for your convenience. They replace the keystrokes Dl 12 Q and 171) 12 payment. BGN mode is discussed more on page 56. [1), respectively. Take another look at the cash-flow schedule for this example:

-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

|

|