HP 30b HP 20b Business Consultant and HP 30b Business Professional User's Guid - Page 61

Volatility, Dividend - purchase

|

View all HP 30b manuals

Add to My Manuals

Save this manual to your list of manuals |

Page 61 highlights

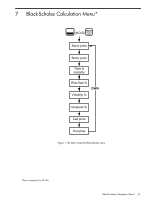

Table 7-1 Item Stock price (input) Strike price (input) Time to maturity (input) Risk free% (input) Volatility % (input) Dividend % (input) Call price (output) Put price (output) Description Current underlying asset price Predetermined price at which the option agrees to buy or sell the underlying asset at maturity. Time remaining until expiration of the option in years. Current risk-free interest rate (for example, the current US Treasury Bond rate). Degree of unpredictable change of the stock price. This is usually approximated by the standard deviation of the variation of the stock price. Estimation of the average dividend yield of the stock as a percentage of its price. Estimated fair market value for a call option at expiration (a call option is the right to purchase the asset at a given price). Estimated fair market value for a put option at expiration (a put option is the right to sell the asset at a given price). Note that if you enter a history of the underlying asset price and its yield in the data menu, = pressing the key on the Volatility % menu item automatically calculates the standard = deviation of the variation of the asset price based on the given data. Pressing in the Dividend % menu item automatically calculates the average dividend as a percent of the asset price. Black-Scholes Calculation Menu* 53

-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

|

|