HP 12C#ABA hp 12c_solutions handbook_English_E.pdf - Page 154

Investment Analysis, Gross Profit.

|

UPC - 492410746430

View all HP 12C#ABA manuals

Add to My Manuals

Save this manual to your list of manuals |

Page 154 highlights

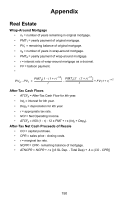

Compounding Periods Different From Payment Periods • C = number of compounding periods per year. • P = number of payments periods per year. • i = periodic interest rate, expressed as a percentage. • r = i / 100, periodic interest rate expressed as a decimal. • iPMT = ((1 + r / C)C/P - 1)100 Investment Analysis Lease vs. Purchase • PMTp = loan payment for purchase. • PMTL = lease payment. • In = interest portion of PMTp for period n. • Dn = depreciation for period n. • Mn = maintenance for period n. • T = marginal tax rate. • k ∑ Net purchasing advantage = -c--c-o--o-s---s-t--tj--f-o-d--f-i--s-l-e-a--a--f--s---id-n---ag----k--(-fn--l--)s---a-----fc--s-o--a-s---(t--f--o,---fx---o-k---w)--F--n---D-i-n---Sg----A-(--n-F---)--F-(1 + i)n n=1 • Cost of owning(n) = PMTp - T(In + Dn) + (1 - T)Mn Break-Even Analysis and Operating Leverage • GP = Gross Profit. • P = Price per unit. • V = Variable costs per unit. • F = Fixed costs. • U = number of Units. • OL = Operating Leverage. • GP = U(P - V) - F • OL = -U----(U---P--(--P-------V-----)V------)---F-- 153

-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

-

161

-

162

-

163

-

164

-

165

|

|