HP 12C#ABA hp 12c_solutions handbook_English_E.pdf - Page 9

Before-Tax Reversions Resale Proceeds, Example, Vacancy Loss. - display problems

|

UPC - 492410746430

View all HP 12C#ABA manuals

Add to My Manuals

Save this manual to your list of manuals |

Page 9 highlights

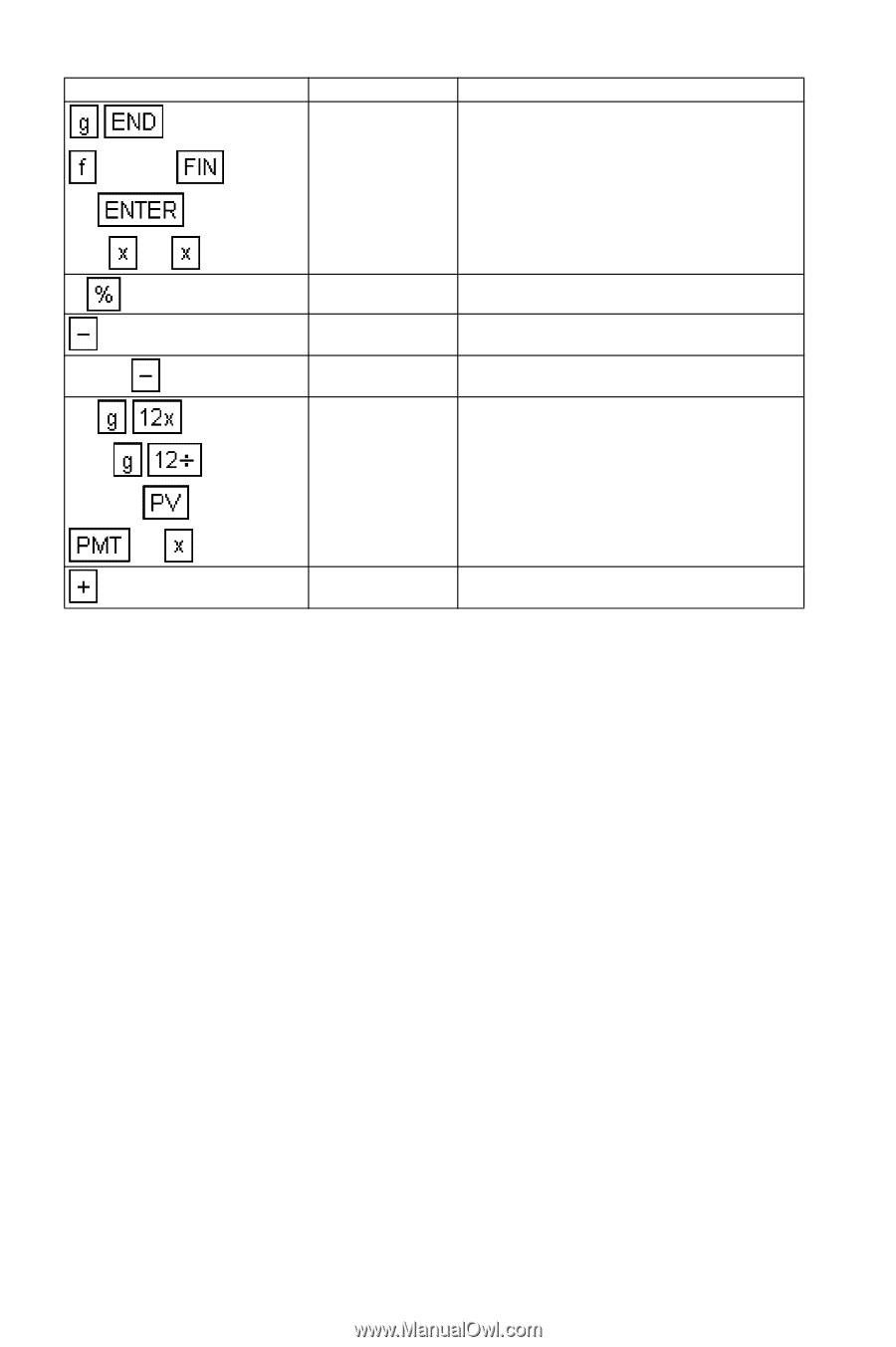

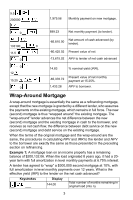

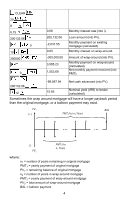

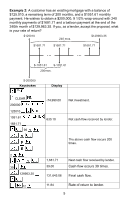

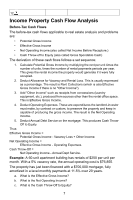

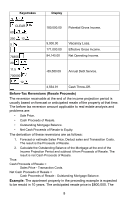

Keystrokes Display CLEAR 60 180,000.00 Potential Gross Income. 250 12 5 9,000.00 171,000.00 Vacancy Loss. Effective Gross Income. 76855 94,145.00 Net Operating Income. 20 11.5 700000 -89,580.09 Annual Debt Service. 12 4,564.91 Cash Throw-Off. Before-Tax Reversions (Resale Proceeds) The reversion receivable at the end of the income projection period is usually based on forecast or anticipated resale of the property at that time. The before tax reversion amount applicable to real estate analysis and problems are: • Sale Price. • Cash Proceeds of Resale. • Outstanding Mortgage Balance. • Net Cash Proceeds of Resale to Equity. The derivation of these reversions are as follows: 1. Forecast or estimate Sales Price. Deduct sales and Transaction Costs. The result is the Proceeds of Resale. 2. Calculate the Outstanding Balance of the Mortgage at the end of the Income Projection Period and subtract it from Proceeds of Resale. The result is net Cash Proceeds of Resale. Thus: Cash Proceeds of Resale = Sales Price - Transaction Costs. Net Cash Proceeds of Resale = Cash Proceeds of Resale - Outstanding Mortgage Balance. Example: The apartment property in the preceding example is expected to be resold in 10 years. The anticipated resale price is $800,000. The 8

-

1

1 -

2

-

3

-

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

|

|