HP 12C#ABA hp 12c_solutions handbook_English_E.pdf - Page 30

Graduated Payment Mortgages - case

|

UPC - 492410746430

View all HP 12C#ABA manuals

Add to My Manuals

Save this manual to your list of manuals |

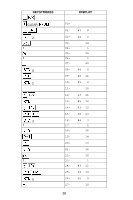

Page 30 highlights

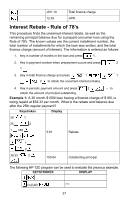

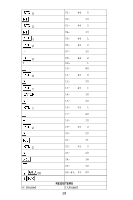

PV: Unused FV: Unused R1: Payment# R3-R.6: Unused 1. Key in the program. PMT: Unused R0: Fin. charge R2: # moths 2. Key in the number of months in the loan and press . 3. Key in the payment number when prepayment occurs and press . 4. Key in the total finance charge and press interest (rebate). to obtain the unearned 5. Key in the periodic payment amount and press principal outstanding. 6. For a new case return to step 2. Keystrokes Display to find the amount of 30 25 5.81 Rebate. 180 39.33 190.84 Outstanding principal. Graduated Payment Mortgages The Graduated Payment Mortgage is designed to meet the needs of young home buyers who currently cannot afford high mortgage payments, but who have the potential of increasing earning in the years on come. Under the Graduated Payment Mortgage plan, the payments increase by a fixed percentage at the end of each year for a specified number of years. Thereafter, the payment amount remains constant for remaining life of the mortgage. The result is that the borrower pays a reduced payment (a payment which is less than a traditional mortgage payment) in the early years, and in the later years makes larger payments than he would with a traditional loan. Over the entire term of the mortgage, the borrower would pay more than he would with conventional financing. Given the term of the mortgage (in years), the annual percentage rate, the loan amount, the percentage that the payments increase, and the number of years that the payments increase, the following HP-12C program determines the monthly payments and remaining balance for each year until the level payment is reached. 29

-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

|

|