HP 12C#ABA hp 12c_solutions handbook_English_E.pdf - Page 157

Forecasting With Exponential Smoothing, Where

|

UPC - 492410746430

View all HP 12C#ABA manuals

Add to My Manuals

Save this manual to your list of manuals |

Page 157 highlights

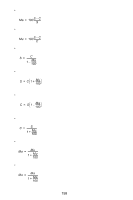

• c = exp 1-n -S----1S----+-1---S-S---3-3---------S--2---22S-----2- • a = exp (---b----------1----)--(---S----2----------S----1---) b(bn - 2 1) • Where S1, S2, and S3 are: • 1t + 1 = St + α-1-- Tt n ∑ S1 = Inyi = n lnc + b( ln a) b--b--n---------1--1- i=1 • 2n ∑ S2 = Inyi = n ln c + bn + 1( ln a) -b-b--n---------1--1- i = n+1 • • a, b and c are determined by solving the three equations above simulta- neously. Forecasting With Exponential Smoothing • a = smoothing constant (0 < a < 1) • Xt = actual current period usage 156

-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

-

164

-

165

|

|

156

•

•

•

Where

S

1

,

S

2

, and

S

3

are:

•

•

•

•

a

,

b

and

c

are determined by solving the three equations above simulta-

neously.

Forecasting With Exponential Smoothing

•

a

= smoothing constant (0 <

a

< 1)

•

X

t

= actual current period usage

c

1

n

--

S

1

S

3

S

2

2

–

S

1

S

3

2S

2

–

+

------------------------------------

exp

=

a

b

1

–

(

)

S

2

S

1

–

(

)

bb

n

1

–

(

)

2

-----------------------------------------

exp

=

S

1

Iny

i

n

c

b

a

ln

(

)

+

ln

=

i

1

=

n

∑

=

b

n

1

–

b

1

–

--------------

S

2

Iny

i

n

c

b

n

1

+

a

ln

(

)

+

ln

=

i

n

1

+

=

2n

∑

=

b

n

1

–

b

1

–

--------------

t

1

+

S

t

1

α

---

T

t

+

=