HP 12C#ABA hp 12c_solutions handbook_English_E.pdf - Page 53

Break-Even Analysis - basics

|

UPC - 492410746430

View all HP 12C#ABA manuals

Add to My Manuals

Save this manual to your list of manuals |

Page 53 highlights

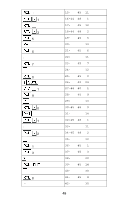

200 1700 200 1700 200 1700 200 1700 300 0 300 0 750 1 3 43 2 -628.09 5th year. -226.44 6th year. -309.48 7th year. -388.81 -1,034.72 -1,080.88 750.00 390.00 239.43 -150.49 8th year. 9th year. 10th year. Buy back. After tax buy back expense. Present value. Net lease advantage. Break-Even Analysis Break-even analysis is basically a technique for analyzing the relationships among fixed costs, variable costs, and income. Until the break even point is reached at the intersection of the total income and total cost lines, the producer operates at a loss. After the break-even point each unit produced and sold makes a profit. Break even analysis may be represented as follows. 52

-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

|

|

52

Break-Even Analysis

Break-even analysis is basically a technique for analyzing the

relationships among fixed costs, variable costs, and income. Until the

break even point is reached at the intersection of the total income and

total cost lines, the producer operates at a loss. After the break-even point

each unit produced and sold makes a profit. Break even analysis may be

represented as follows.

200

1700

-628.09

5th year.

200

1700

-226.44

6th year.

200

1700

-309.48

7th year.

200

1700

-388.81

8th year.

300

0

-1,034.72

9th year.

300

0

-1,080.88

10th year.

750

750.00

Buy back.

1

3

390.00

After tax buy back expense.

43

239.43

Present value.

2

-150.49

Net lease advantage.